15 Kaloaloa Way #7A, Wailuku, Maui TownHome For Sale

Iliahi at Kehalani is a very pretty, well cared for complex with just 4 Townhomes per building spread fairly far apart, parking right outside the unit one covered and one uncovered, sufficient visitor parking, bar-b-que & picnic table areas, park-like setting, and architectural features such as high ceilings; vaulted in the primary bedroom, wider staircase, ample kitchen cabinets, storage closets including a large walk-in storage on the lanai, primary suite with walk-in closet and ensuite bath, & a second walk in closet in another bedroom. This Townhome End Unit A is staggered out on a hill so it offers greater privacy with surrounding manicured treetops and the adjacent driveway’s open space. The extra walls of windows upstairs and downstairs is light-filled & on the side where the cooling trade winds flow providing the refreshing cross breeze both inside and out! This Home looks barely lived in as it was utilized as a Second Home for the past 10 years. Some of the upgrades include luxury vinyl plank flooring with high quality carpet on the staircase. This lanai is extra private, boasts Haleakala Views, and is a peaceful place to begin and end your day with your beverage of choice. Bring out the luau table & chairs for the lawn area in front of the lanai and enjoy an alfresco gathering. This home is squeaky clean, tastefully furnished, and turnkey with the furnishings, housewares, linens, art & decorations, tools and ladders, beach gear, etc. all included. Kehalani is one of the most sought out areas of Central Maui, loved because of the cooler climate of the foothills of the West Maui Mountains, tree lined sidewalks, park, and convenience to just about everything.

MLS No. 403437

Visit my website at www.FindMauiProperty.com to Search the Maui MLS and Find Useful Resources

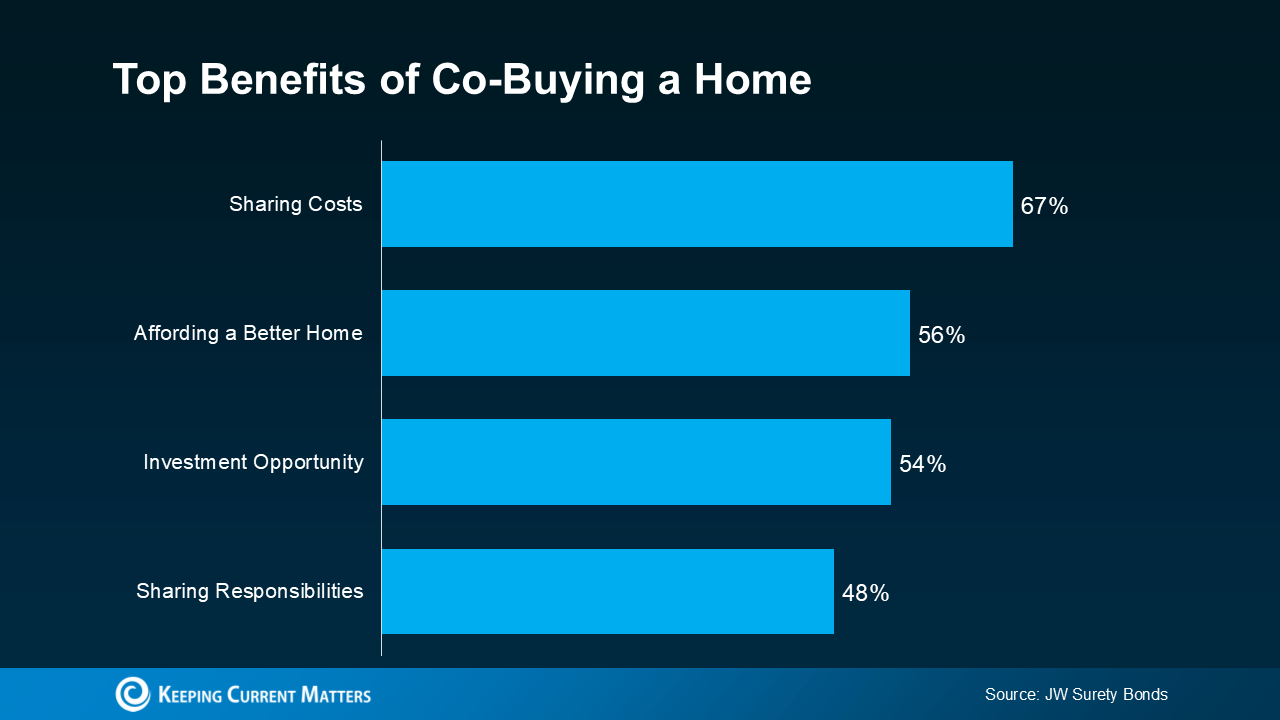

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

Sharing Costs (67%): From saving for a down payment to managing monthly payments, buying a home is a big financial step. When you co-buy, you split these costs, making it easier to afford a home.

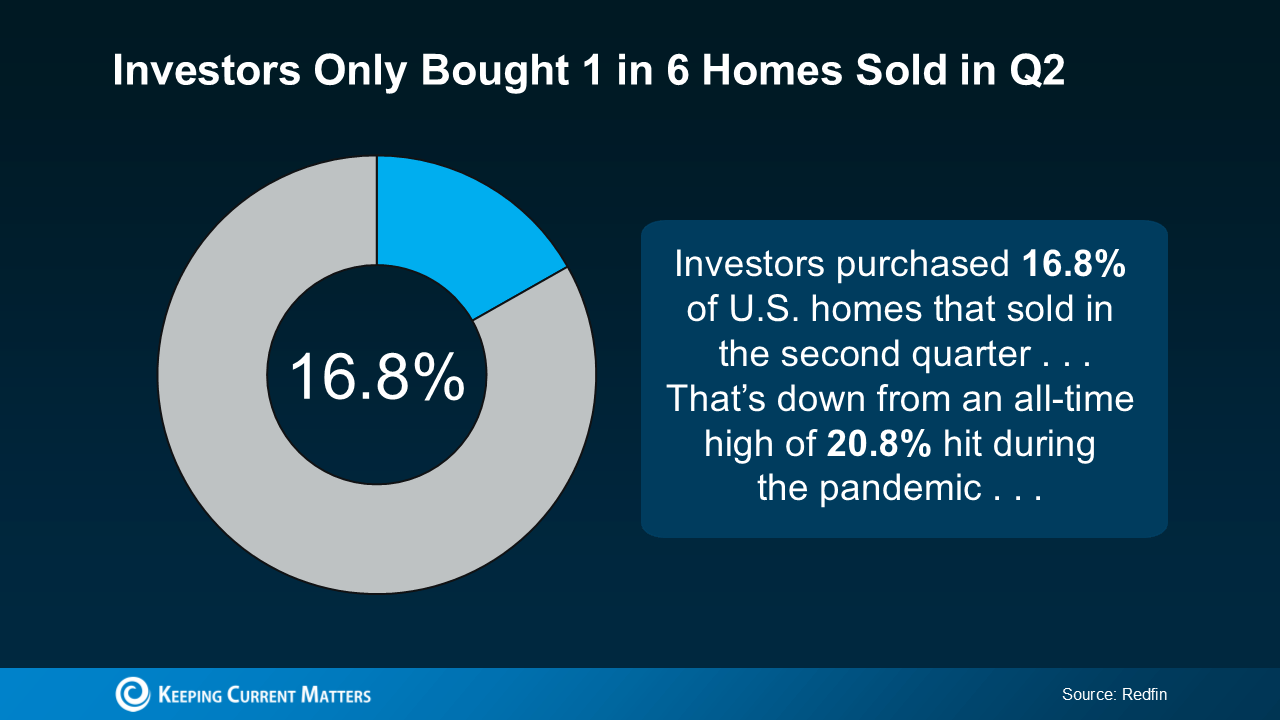

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.