A real estate sign is shown on a property in 2018. As prices continue to set new records and “affordable” homes grow more out of reach, county officials are searching for ways to help local residents afford a place to live, including updating current county rent and sales price guidelines. The Maui News / MATTHEW THAYER photo

While qualifying for a mortgage in Maui County is already a challenging feat amidst the housing crisis, affording the payments after the fact and for the long term is another.

“The numbers of those that are qualified are low, and those who do qualify, they are also getting priced out because (the housing model) is not a long-term, equitable plan,” said Keaka Aumua, a community service specialist at Hawaiian Community Assests’ Maui Financial Opportunity Center. “While you may get a mortgage, you’re going to get priced out and you may not be able to afford it long term.”

Updating the county’s rent and sales price guidelines to include principal, interest, taxes, insurance, mortgage insurance and homeowner association fees capped at 31 percent of the homeowner’s gross monthly income was one of the proposed solutions discussed during the Maui County Council’s Affordable Housing Committee meeting on Monday.

“We have all heard from residents over and over again, and justifiably, that even Maui’s affordable homes are not affordable to them,” said committee Chairperson Gabe Johnson, who is working to promote equity and access to affordable mortgages for all residents.

Maui County’s housing market continues to set new records. The median sales price for a single-family home in April reached $1,242,500, a new record and a 27.4 percent increase over the median price of $975,000 a year ago.

Only about 28 percent of the Maui Financial Opportunity Center clientele — lower- to moderate-income families — qualify for mortgages, while 72 percent have not yet qualified even after services, education and support, Aumua said during her presentation to the committee.

Due to the rising costs of living, many individuals “get priced out” before the purchasing process even starts, while others who may have enough income and assets initially for a down payment and to secure a mortgage loan eventually find it’s “not enough to keep these families in their home long term.”

“This ends up setting these families up for failure,” Aumua added.

For example, a family of four with about 50 percent of the area median income ($57,000) could expect to pay about $27,000, which does not include other expenses, like interest, equated monthly installment fees or HOAs, which often leaves them “struggling to use their remaining amount of less than $2,000 toward all other expenses,” such as child care, food, gas and utilities.

That’s not to mention any emergencies that may arise, like a car accident, medical bills or loss of income.

“A home becomes more of a burden than a blessing due to unforeseen circumstances in an effort to keep up with the costs, and this translates into a loss of home security,” she added.

Faith Armanini of Homebridge Financial Services said “I don’t think anyone can live on 16 percent of their income for all the fees that they have.”

Armanini, who sees debt ratios as high as 49 percent of an individual’s gross income when investing in home, said that any average two-person household won’t be able to afford one under the current U.S. Department of Housing and Urban Development guidelines.

“Personally, I would choke on a payment of $3,688 a month and for us to expect a husband and wife working and paying that amount, is just, for me, unfair that they have to pay that amount,” she said.

Based on what Maui Financial Opportunity Center sees, Aumua suggested lowering prices between $150,000 to $200,000 for an apartment for low- to moderate-income working families, and $350,000 to $450,000 for single-family homes.

“I understand that there are so many other factors, and again, moving those factors aside and asking the question, ‘What is an ideal price for families of this low to moderate income bracket?’ These would be the prices,” Aumua said.

There are two factors that determine affordable home prices, including area median income brackets in Maui County and a formula calculated by the county’s Department of Housing and Human Concerns based on HUD standards.

“By simply changing the formula we use based on the federal program’s standards, we can make affordable homeownership accessible to more people,” Johnson said.

A policy priority under the Comprehensive Affordable Housing Plan calls for updating the county’s rent and sales price guidelines to promote equity and access to affordable mortgage financing for all residents.

Johnson said that the county imposes sales price guidelines that limit a homeowner’s monthly payment of principal and interest to 28 percent of their gross monthly income and do not account for typical monthly mortgage costs, including taxes, insurance, mortgage insurance and homeowners association fees, which is “problematic.”

Maui County’s sales price guidelines differ from mainstream mortgage standards and federal programs, like U.S. Department of Agriculture and Federal Housing Administration loans, limiting local families’ ability to use these federal programs with low and no down payment requirements to purchase homes.

This is why the county needs to update the policy, Johnson said. The plan recommends capping the maximum monthly payment of principal, interest, taxes, insurance, mortgage insurance and homeowner association fees at 31 percent of the homebuyer’s gross monthly income.

To address concerns by developers who cannot build and profit off low-cost homes, Johnson and other council members said it’s important to implement legislation to expand the uses of the Affordable Housing Fund before changes to the price guidelines are made.

Funds could help to subsidize the development of more homes and “tackle this crisis,” he said.

“We have to get real about what our workforce can afford, so that we can actually attempt to solve our housing problem,” he added.

While developing a new policy, Council Member Tasha Kama said it will be important to begin by targeting the low- to moderate-income groups as well as include developers in the conversation.

“If we go into this discussion with everything on the table, be as transparent as we possibly can with everybody,” Kama said. “I think at some point in time, we’re going to have to realize that some people are not going to be homeowners at this time, but we can certainly help bring them up to that place.”

If units are going to be subsidized, Council Member Kelly King suggested that there be a balance of how much taxpayers get back, as well as “getting creative” if the council decides to look into deed restrictions, paybacks, perpetuity policies and so forth.

Council Member Tamara Paltin said she would like the new policy to support homeownership in perpetuity, too, and also protect growing families who wish to expand or upsize their home or to include funding that could lower interest rates.

Council Chairperson Alice Lee said they should consider building on county lands, outsourcing projects, looking into cheaper projects, possibly expanding funds for affordable housing projects or offering land to allow working families to build their own homes.

“I think if we keep our minds flexible and open, I think we’ll be able to come up with a wide range of solutions,” Lee said.

* Dakota Grossman can be reached at dgrossman@mauinews.com.”

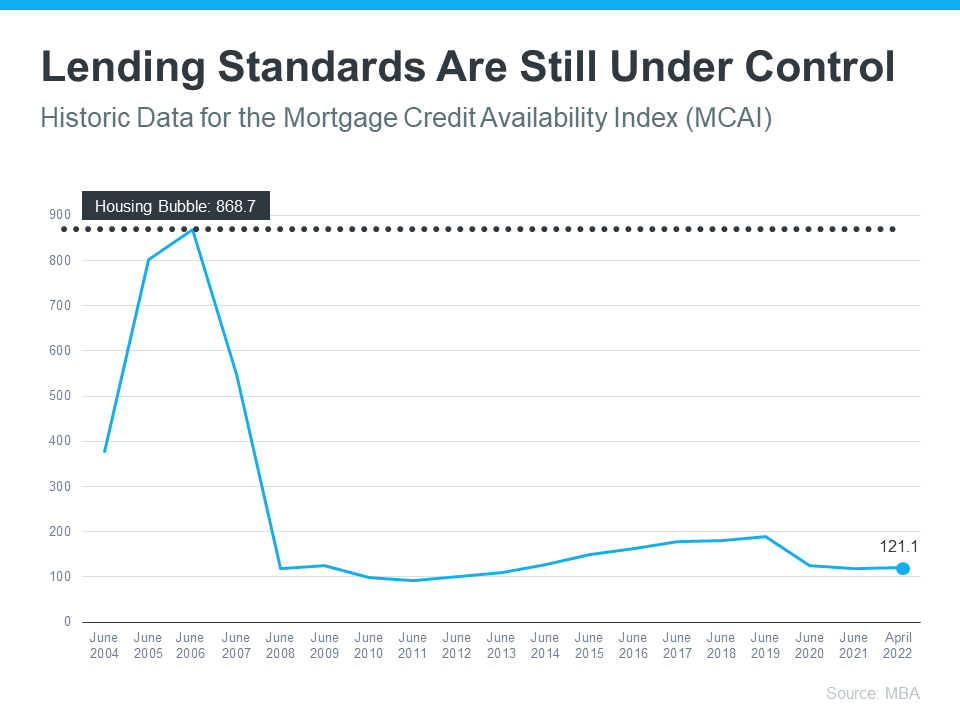

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006.

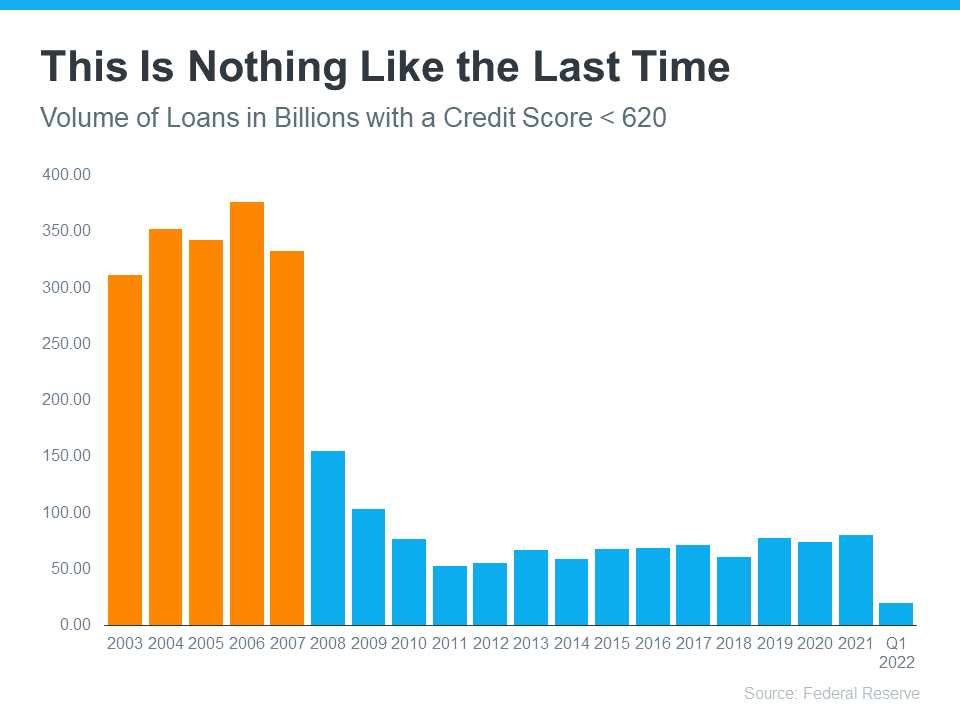

As the graph shows, the index stood at about 400 in 2004. Mortgage credit became more available as the housing market heated up, and then the index passed 850 in 2006. When the real estate market crashed, so did the MCAI as mortgage money became almost impossible to secure. Thankfully, lending standards have eased somewhat since then, but the index is still low. In April, the index was at 121, which is about one-seventh of what it was in 2006. In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

In 2006, buyers with a score under 620 received $376 billion dollars in loans. In 2021, that number was only $80 billion, and it’s only $20 billion in the first quarter of 2022.

![Bright Days Are Ahead When You Move Up This Summer INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/26132018/20220527-MEM-1046x1913.png)

![Don’t Let Rising Inflation Delay Your Homeownership Plans INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2022/05/18153723/20220520-MEM-1046x2334.png)