If you’ve been keeping an eye on the housing market over the past couple of years, you know sellers have had the upper hand. But is that going to shift now that inventory is growing? Here’s a breakdown of what you need to know.

What Is a Balanced Market?

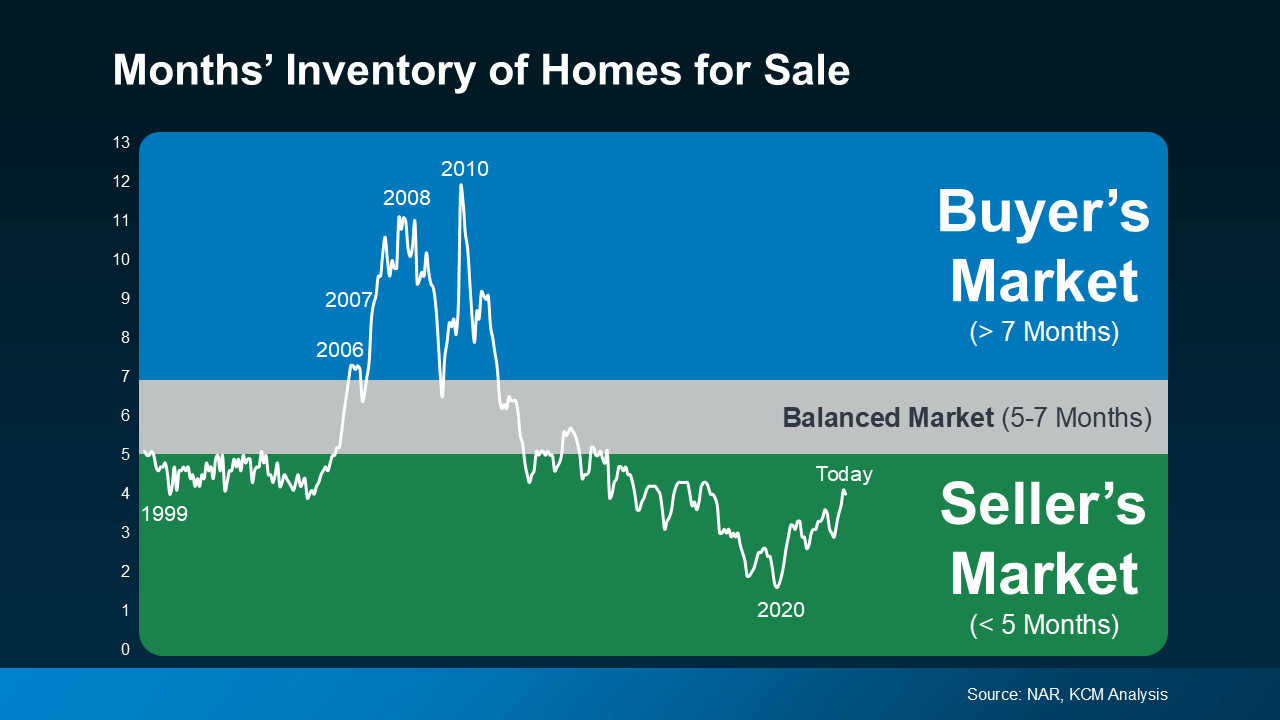

A balanced market is generally defined as a market with about a five-to-seven-month supply of homes available for sale. In this type of market, neither buyers nor sellers have a clear advantage. Prices tend to stabilize, and there’s a healthier number of homes to choose from. And after many years when sellers had all the leverage, a more balanced market would be a welcome sight for people looking to move. The question is – is that really where the market is headed?

After starting the year with a three-month supply of homes nationally, inventory has increased to four months. That may not sound like a lot, but it means the market is getting closer to balanced – even though it’s not quite there yet. It’s important to note this increase in inventory is not leading to an oversupply that would cause a crash. Even with the growth lately, there’s still nowhere near enough supply for that to happen.

The graph below uses data from the National Association of Realtors (NAR) to give you an idea of where inventory has been in the past, and where it’s at today:

For now, this is still seller’s market territory – it’s just not as frenzied of a seller’s market as it’s been over the past few years. As Mark Fleming, Chief Economist at First American, says:

“The faster housing supply increases, the more affordability improves and the strength of a seller’s market wanes.”

What This Means for You and Your Move

Here’s how this shift impacts you and the market conditions you’ll face when you move. Lawrence Yun, Chief Economist at NAR, explains:

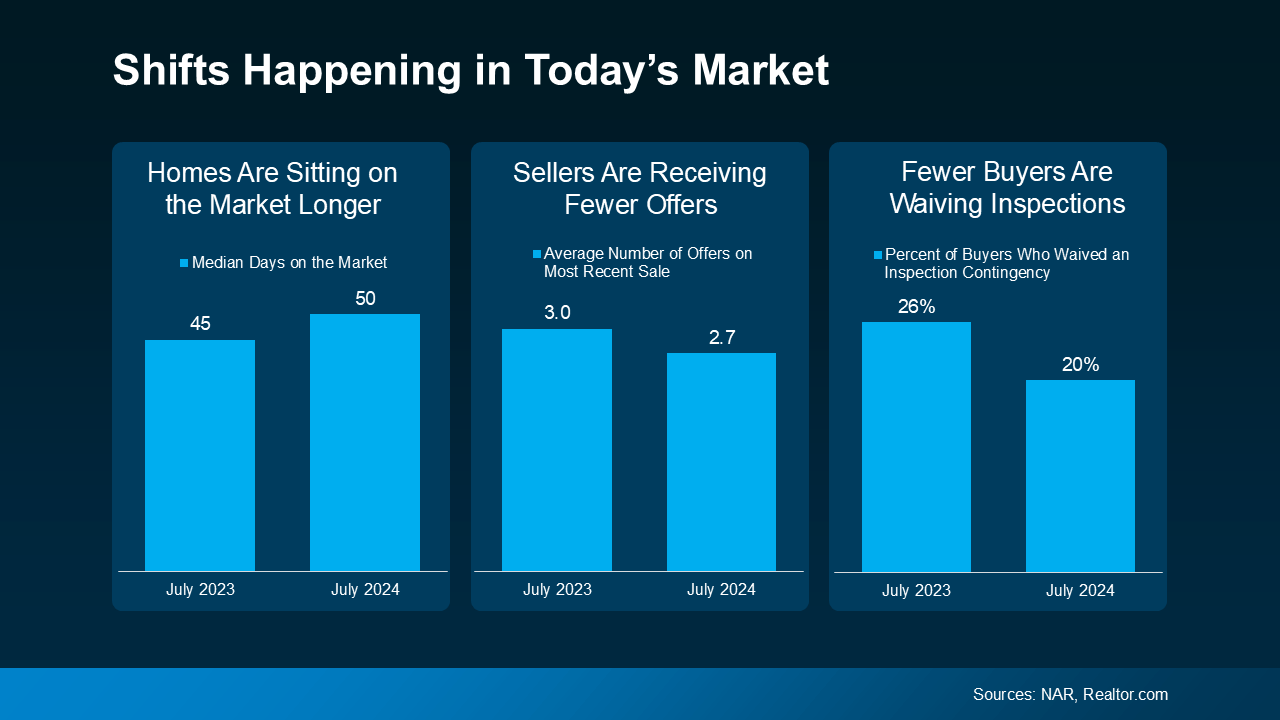

“Homes are sitting on the market a bit longer, and sellers are receiving fewer offers. More buyers are insisting on home inspections and appraisals, and inventory is definitively rising on a national basis.”

The graphs below use the latest data from NAR and Realtor.com to help show examples of these changes:

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to price your house right if you want it to sell. If you don’t, buyers might choose better-priced options.

Sellers Are Receiving Fewer Offers: As a seller, you might need to be more flexible and willing to compromise on price or terms to close the deal. For buyers, you could start to face less intense competition since you have more options to choose from.

Fewer Buyers Are Waiving Inspections: As a buyer, you have more negotiation power now. And that’s why fewer buyers are waiving inspections. For sellers, this means you need to be ready to negotiate and address repair requests to keep the sale moving forward.

How a Real Estate Agent Can Help

But this is just the national picture. The type of market you’re in is going to vary a lot based on how much inventory is available. So, lean on a local real estate agent for insight into how your area stacks up.

Whether you’re buying or selling, understanding how the market is changing gives you a big advantage. Your agent has the latest data and local insights, so you know exactly what’s happening and how to navigate it.

Bottom Line

The real estate market is always changing, and it’s important to stay informed. Whether you’re buying or selling, understanding this shift toward a balanced market can help. If you have any questions or need expert advice, don’t hesitate to reach out to a local real estate agent.

Visit my website www.FindMauiProperty.com to search the Maui MLS and Find Useful Resources.

“Queen Kaʻahumanu Center change of zoning gets final Council approval for redevelopment

By Brian Perry August 28, 2024 · 4:38 AM HST * Updated August 28, 2024 · 4:39 AM

758Shares

Queen Kaʻahumanu Center’s front entrance is located off of Kaʻahumanu Ave. in Kahului. Maui County Council members approved land use bills on second-and-final reading Tuesday to make way for possible mixed-use redevelopment of the property. PC: Brian Perry

Maui County Council members approved on second-and-final reading Tuesday land use measures to pave the way for redevelopment of Queen Kaʻahumanu Center as it struggles amid a nationwide decline in brick-and-mortar shopping malls. Bills 67 and 68 advance to Mayor Richard Bissen for final action.

The measures provide for a Wailuku-Kahului Community Plan amendment for 6.75 acres and a change of zoning from M-2 Heavy Industrial District to B-3 Central Business District for 33.8 acres for the Queen Kaʻahumanu Community Center revitalization and infill project.

In June, representatives of the mall owners said the land use bills would allow them to proceed with “evolution” of the center and evaluate opportunities based on community needs. They are considering a mixed-use development, including residential, retail, office, service, open and green space.

The mall’s current heavy industrial zoning does not allow for multifamily residential uses.

No specific development plans have been proposed. Future plans will need to be reviewed by the county Urban Design Review Board, and they’ll need a special management area permit from the Maui Planning Commission.

In 2022, 700 large shopping malls closed in the United States, due in part to the popularity of convenient online shopping with giants such as Amazon.

Former Queen Kaʻahumanu anchor tenant Sears shuttered its retail operations at the mall in November 2021. Consolidated Theatres closed its Kaʻahumanu movie theaters in July 2023, after nearly 30 years. And, in the not-too-distant future, one of the center’s two Macy’s retail stores will close and consolidate into a single store, according to a June 5 presentation by mall owners and consultants to members of the Maui County Council’s Housing and Land Use Committee.

In June, tenants with long-term leases occupied only 41% of the center; the remaining 51% was either vacant or at risk of becoming vacant.

The center property is owned by GSMS 2014-GC26 West Kaʻahumanu Ave. LLC. The property manager is Pacific Retail Capital Partners.

In other action Tuesday, Council members approved on second-and-final reading Bill 28. The bill, which advances to the mayor for action, amends the state land use district boundary from agricultural to urban for nearly 11.5 acres in Waiehu for the Hale Mahaolu Ke Kahua affordable housing project.

Project plans call for building 120 one-, two- and three-bedroom units for families at or below 60% of Maui County’s area median income. The project is being developed as a partnership with Hale Mahaolu, Maui Economic Opportunity Inc. and High Ridge Costa.

Before voting, council members heard public testimony disputing ownership of the property. Council Chair Alice Lee said that matter should be settled in the courts.

MEO maintains it has clear title to the property, confirmed in a 2nd Circuit Court ruling that it has “possessory and title interest” in the land and that title can be traced through King Lunalilo and a royal patent grant.

The final Council vote on final approval of the bill was 5-4, with “aye” votes from Lee and Council Members Tasha Kama, Yuki Lei Sugimura, Tom Cook and Nohelani Uʻu-Hodgins. “Nay” votes came from Keani Rawlins-Fernandez, Tamara Paltin, Shane Sinenci and Gabe Johnson.

MEO Chief Executive Officer Debbie Cabebe thanked the County Council for voting to amend the property’s state land use district classification for a project that will provide “120 badly needed rental units for low income and working families on Maui. There is a desperate need for affordable places to live, especially since the wildfires of Aug. 8, 2023.”

“While there is an outcry for affordable units, we acknowledge and understand the spirited debate over the Ke Kahua housing development,” she said. “With today’s decision, we now will be able to build a project that will bring stable, long-term housing to our local families.”

The Council also adopted a resolution honoring Capt. Riley Coon and the Trilogy Excursions ʻOhana for helping save the lives of Lahaina wildfire survivors who had escaped into the ocean to flee wildfire flames on Aug. 8, 2023.”

Visit my website: www.FindMauiProperty.com to search the Maui MLS and Find Useful Resources

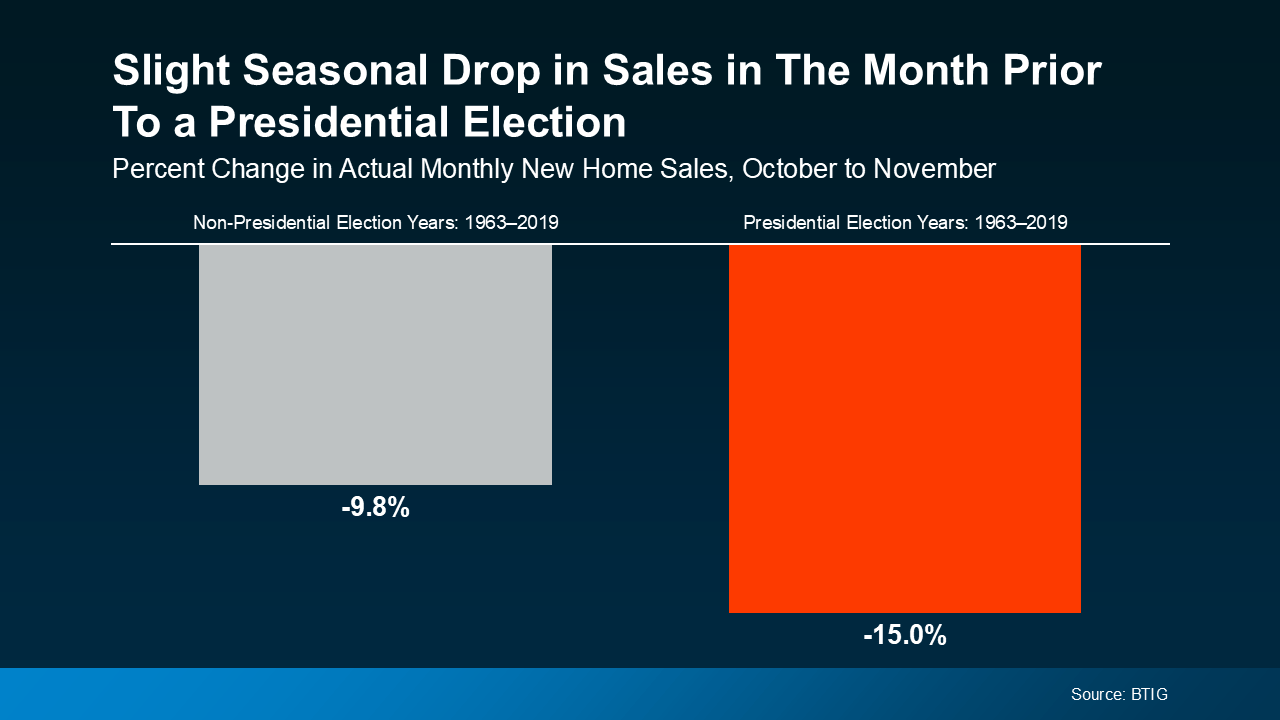

It’s no surprise that the upcoming Presidential election might have you speculating about what’s ahead. And those unanswered thoughts can quickly spiral, causing fear and uncertainty to swirl through your mind. So, if you’ve been considering buying or selling a home this year, you’re probably curious about what the election might mean for the housing market – and if it’s still a good time to make your move.

Here’s the good news that may surprise you: typically, Presidential elections have only had a small, temporary impact on the housing market. But your questions are definitely worth answering, so you don’t have to pause your plans in the meantime.

Here’s a look at decades of data that shows exactly what’s happened to home sales, prices, and mortgage rates in previous Presidential election cycles, so you can move forward with the facts as you weigh the pros and cons of your homeownership decision.

Home Sales

In the month leading up to a Presidential election, from October to November, there’s typically a slight slowdown in home sales(see graph below):

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

Historically, home sales bounce right back and continue to rise the following year.

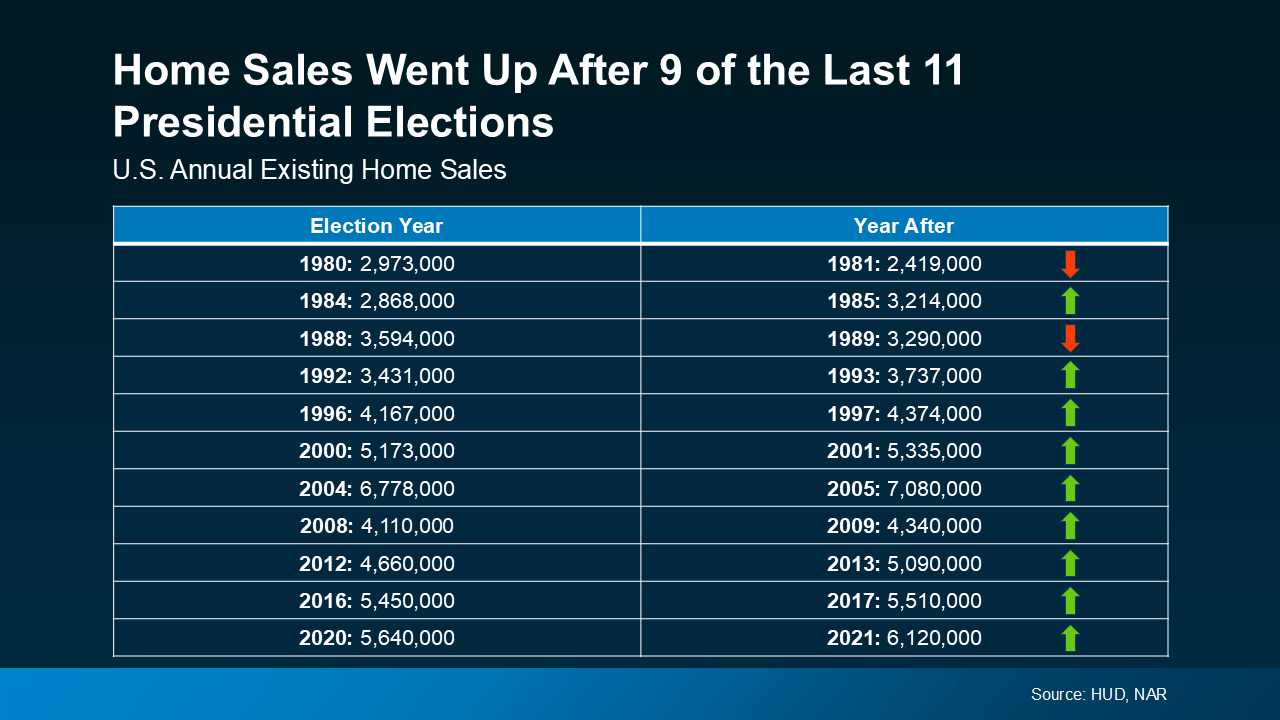

You may also be wondering about home prices. Do prices come down during election years? Not typically. As residential appraiser and housing analyst Ryan Lundquist notes:

“An election year doesn’t alter the price trend that is already happening in the market.”

Home prices generally rise over time, regardless of an election cycle. So, based on what history shows, you can expect the current pricing trend in your local market to likely continue, barring any unusual market or economic circumstances.

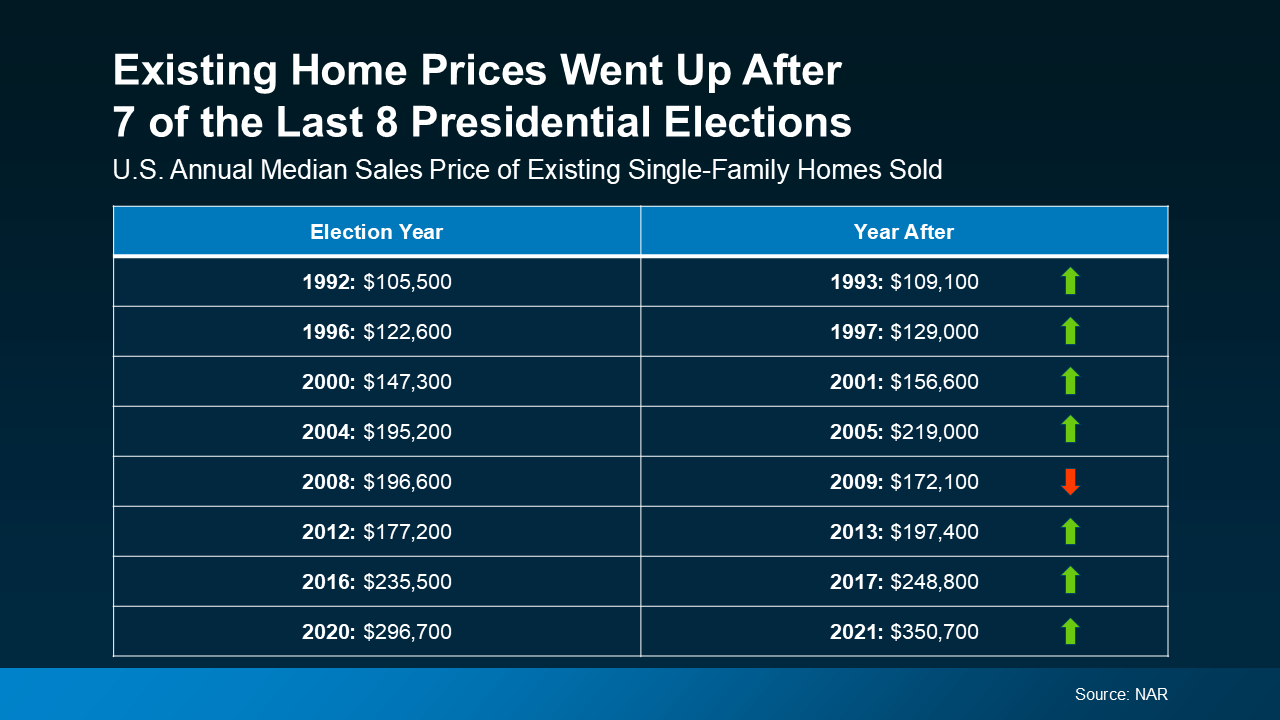

The latest data from NAR reveals that after 7 of the last 8 Presidential elections, home prices increased the following year (see chart below):

The one outlier was from 2008 to 2009, which was during the height of the housing market crash. That was certainly not a typical year. Today’s market, however, is much more resilient. And while prices are moderating nationally, they aren’t on an overall decline.

Mortgage Rates

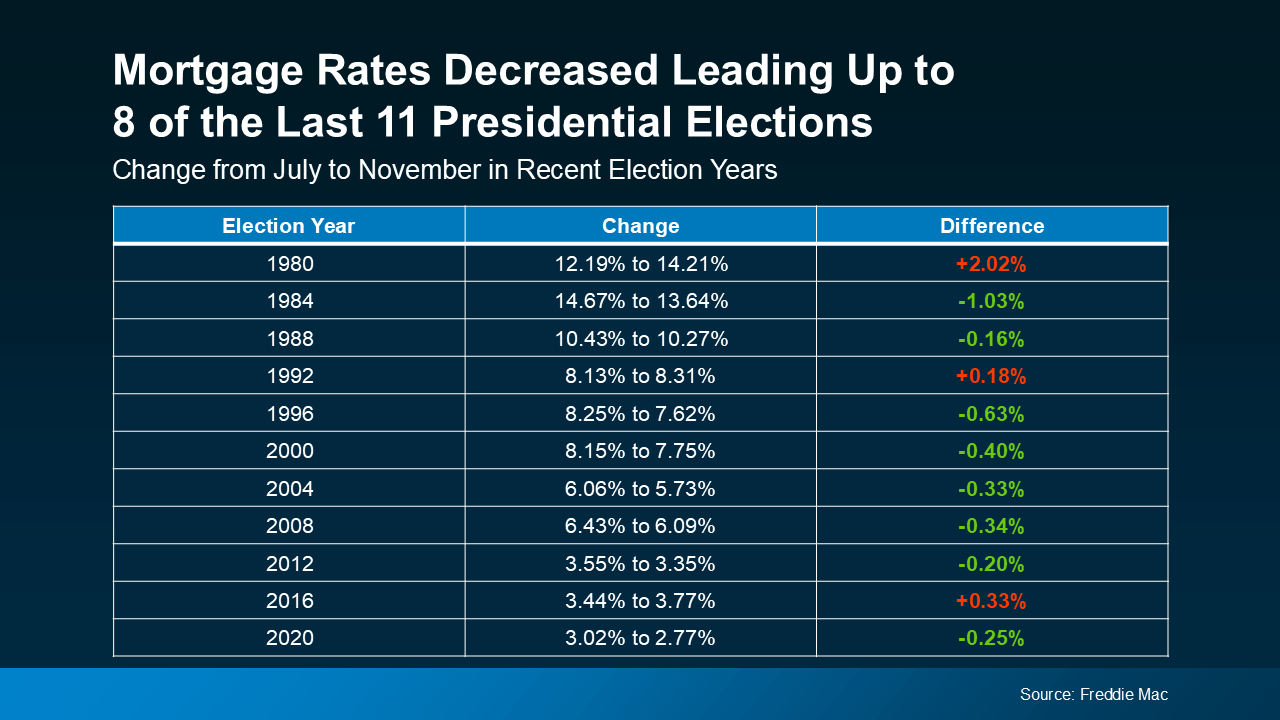

And the third thing that’s likely on your mind is mortgage rates, since they impact your monthly payment if you’re financing a home. Looking at the last 11 Presidential election years, data from Freddie Mac shows mortgage rates decreased from July to November in 8 of them (see chart below):

And this year, we’ve already started to see that happen. Most experts also forecast mortgage rates will ease slightly throughout the rest of 2024. If that happens – and all signs right now indicate it should – this year will continue to follow the trend of declining rates. So, if you’re looking to buy a home in the coming months, this could be great news for your purchasing power.

What This Means for You

What’s the big takeaway? While Presidential elections do have some impact on the housing market, the effects are usually minimal. As Lisa Sturtevant, Chief Economist at Bright MLS, says:

“Historically, the housing market doesn’t tend to look very different in presidential election years compared to other years.”

For most buyers and sellers, elections don’t have a major impact on their plans.

Bottom Line

While it’s natural to feel a bit uncertain during an election year, history shows the housing market remains strong and resilient. And this means you don’t have to pause your plans in the meantime. For help navigating the market during this election cycle, reach out to a local real estate agent.

Visit my website at www.FindMauiProperty.com to search the Maui MLS and Find Helpful Resources.

Via State of Hawaii, Dept. of Commerce and Consumer Affairs:

“JOSH GREEN, M.D.

GOVERNOR KE KIAʻĀINA

GOVERNOR GREEN SIGNS EMERGENCY PROCLAMATION TO ADDRESS CONDO INSURANCE CRISIS

FOR IMMEDIATE RELEASE

August 7, 2024

HONOLULU — Governor Josh Green, M.D., today signed an emergency proclamation aimed at stabilizing Hawai‘i’s volatile condominium insurance market, which has seen unprecedented rate increases due to a hardening global insurance industry and recent increase of catastrophic events around the world.

Hawai‘i’s property insurance market faces significant challenges due to its small size, high real estate costs and unique risk profile. The wildfire in Maui has highlighted these issues for our state, leading to skyrocketing insurance rates for condos, some increasing by as much as 1,000%. With the possibility of similar rate hikes for townhouses, immediate action is required to protect Hawaiʻi homeowners and maintain market stability.

Governor Green emphasized the urgency of the situation, stating, “The recent surge in condo insurance rates is placing an unbearable burden on homeowners across our state. This emergency proclamation is a critical step to stabilize our insurance market and protect our residents from further financial strain. By working closely with industry experts, federal partners and legislative leaders, we aim to ensure that Hawai‘i remains a viable and secure place to live, even in the face of global insurance challenges. Our commitment is to safeguard the interests of our communities and provide stability for people living and working in Hawaiʻi.”

Governor Green established a Joint Executive and Legislative Task Force to monitor the insurance market, implement short-term fixes and recommend emergency changes or legislative proposals. The task force is headed by State Insurance Commissioner Gordon I. Ito, House Speaker, Representative Scott K. Saiki (D-25, Ala Moana, Kaka‘ako, Downtown) and Senate Leader Senator Jarrett Keohokalole, (District 24, Kāne‘ohe, Kailua), with members from the insurance, mortgage lending and real estate industries.

This emergency proclamation will lead to providing additional options for condominium associations to purchase hurricane and property insurance for their buildings including the following:

Allows loans to be made to the Hawaiʻi Hurricane Relief Fund (HHRF) and the Hawaiʻi Property Insurance Association to facilitate issuance of hurricane and property insurance policies to condo associations

Allows HHRF to issue hurricane insurance policies for large condominium buildings and set its own coverage limits

“I want to thank the Governor for accepting the recommendation of the Insurance Task Force and recognizing that we are in a state of emergency,” said House Speaker Saiki. The Emergency Proclamation will allow the Administration to help Hawaiʻi’s condominiums access a layer of property insurance coverage. We know that condominium owners are frustrated and worried about the rising cost of property insurance and our Task Force will continue to work to identify potential solutions.

The Task Force met and this emergency proclamation was the result of their work and evaluation which included:

Examining the insurance marketplace for trouble spots and urgent changes in insurers’ rates, refusals to write policies, or market exits.

Determining existing legal authority for immediate fixes.

Identifying statutory changes that can be waived via emergency proclamation or require legislative action, making recommendations for such actions.

Engaging with federal stakeholders like Fannie Mae and Freddie Mac to support these efforts.

An executed copy of the Proclamation can be found here.

The letter from the Joint Executive and Legislative Task Force is here.

“Maui County vacation rental occupancy at 53% as demand remains lower than 2023

August 25, 2024 · 8:00 AM HST

Koa Lagoon in Kīhei. PC: Brian Perry

Despite having the most vacation rental units in the state, Maui County’s demand and occupancy were down double-digits compared to last year and 2019, before the COVID-19 pandemic, according to a report for July by the Department of Business, Economic Development & Tourism.

The county had 266,400 available unit nights in July—7.1% fewer than pre-pandemic levels but 6.6% more than in 2023. Demand, however, was just 141,400 nights, down 39% from 2019 and 11% from last year, leading to a 53.1% occupancy rate—a 28.4-point drop from 2019 and 10.5 points lower than 2023.

The average daily rate for vacation rentals was $388, up 8.2% from 2023 and 64.8% from 2019. For comparison, Maui County hotels reported a $573 average rate and 60.5% occupancy for July 2024.

O‘ahu vacation rental supply was 219,400 available unit nights, followed by Hawai‘i Island’s 214,500 and Kaua‘i’s 135,800 unit nights. Vacation rentals across the state reported increases in supply and demand, with lower occupancy rates in July 2024 compared to July 2023.

In July 2024, the total monthly supply of statewide vacation rentals was 836,100 unit nights (+5.5% vs. 2023, -7.6% vs. 2019) and monthly demand was 459,900 unit nights (+1.1% vs. 2023, -34.7% vs. 2019). This combination resulted in an average monthly unit occupancy of 55% (-2.3 percentage points vs. 2023, -22.8 percentage points vs. 2019) for July. Occupancy for Hawai‘i’s hotels was 78.4% in July 2024.

Average daily rates (ADR) for vacation rentals were up across all counties when compared to July 2023 and 2019. Statewide, the ADR was $334 (+9.8% vs. 2023, +61.0% vs. 2019). By comparison, the ADR for hotels was $573 in July 2024. It is important to note that unlike hotels, units in vacation rentals are not necessarily available year-round or each day of the month and often accommodate a larger number of guests than traditional hotel rooms.

The data in DBEDT’s Hawai‘i Vacation Rental Performance Report specifically excludes units reported in DBEDT’s Hawai‘i Hotel Performance Report and Hawai‘i Timeshare Quarterly Survey Report. A vacation rental is defined as the use of a rental house, condominium unit, private room in a private home, or shared room/space in a private home. This report does not determine or differentiate

Visit my website: www.FindMauiProperty.com to search the Maui MLS and Find Useful Resources.

Over the past couple of years, a lot of people have had a hard time buying a home. And while affordability is still tight, there are signs it’s getting a little better and might keep improving throughout the rest of the year. Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Housing affordability is improving ever so modestly, but it is moving in the right direction.”

Here’s a look at the latest data on the three biggest factors affecting home affordability: mortgage rates, home prices, and wages.

1. Mortgage Rates

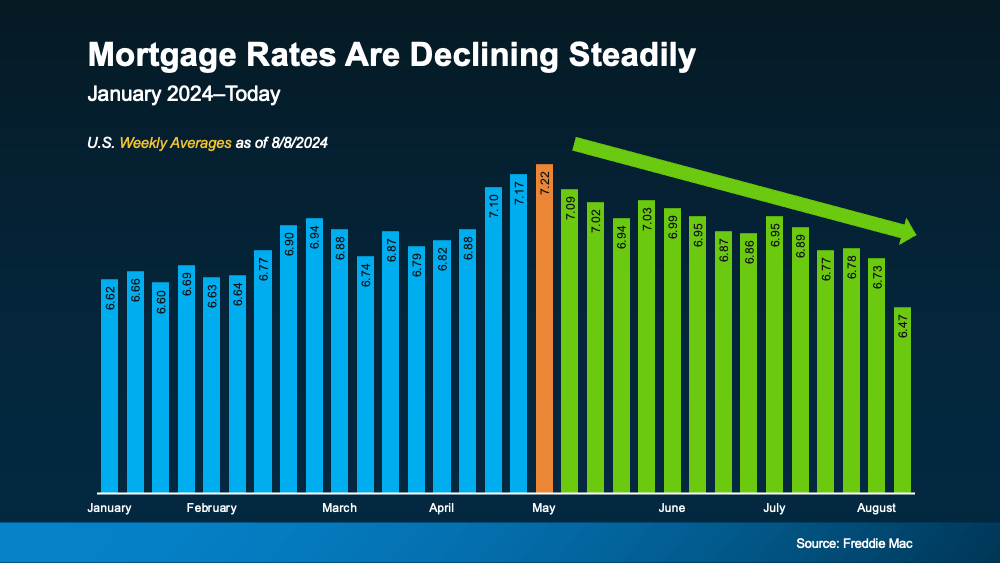

Mortgage rates have been volatile this year, bouncing around from the mid-6% to low 7% range. But there’s some good news. Data from Freddie Mac shows rates have been trending down overall since May (see graph below):

Mortgage rates have improved lately in part because of recent economic, employment, and inflation data. Moving forward, some rate volatility is to be expected. But if future economic data continues to show signs of cooling, experts say mortgage rates could keep going down.

Even a small drop can help you out. When rates decline, it’s easier to afford the home you want because your monthly payment will be lower. Just don’t expect them to go back down to 3%.

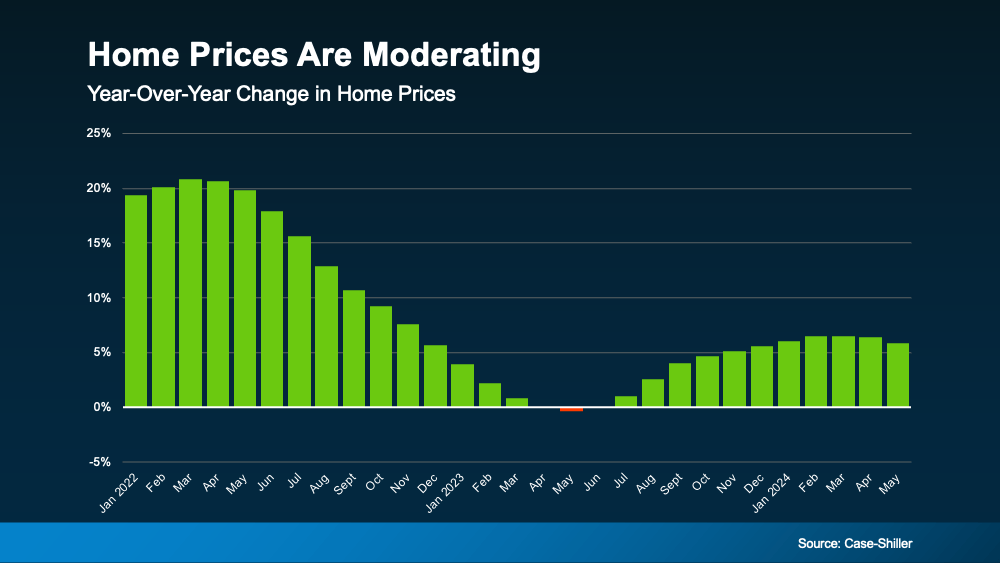

2. Home Prices

The second big thing to think about is home prices. Nationally, they’re still going up this year, but not as fast as they did a couple of years ago. The graph below uses home price data from Case-Shiller to illustrate that point:

If you’re thinking about buying a home, slower price growth is good news. Home prices went up a lot during the pandemic, making it hard for many people to buy. Now, with prices rising more slowly, buying a home may feel less out of reach. As Odeta Kushi, Deputy Chief Economist at First American, says:

“While housing affordability is low for potential first-time home buyers, slowing price appreciation and lower mortgage rates could help – so the dream of homeownership isn’t boarded up just yet.”

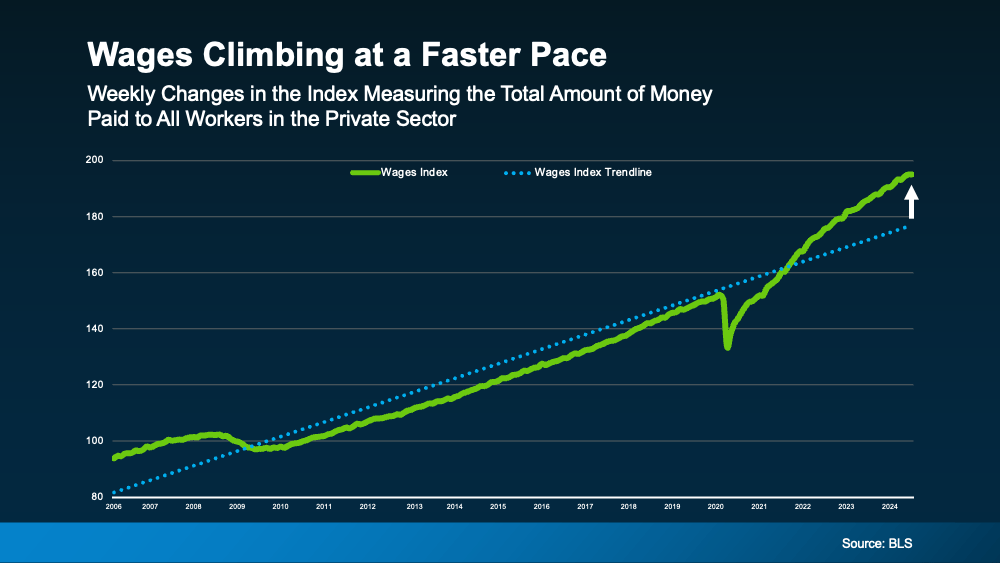

3. Wages

Another factor helping with affordability is rising wages. The graph below uses data from the Bureau of Labor Statistics (BLS) to show how wages have increased over time:

Look at the blue dotted line. It shows how wages usually go up in a typical year. On the right side of the graph, you’ll see wages are rising even faster than normal right now – that’s the green line.

This helps you because if your income increases, it’s easier to afford a home. That’s because you won’t have to spend as much of your paycheck on your monthly mortgage payment.

Bottom Line

When you put all these factors together, you see mortgage rates are trending down, home prices are rising more slowly, and wages are going up faster than usual. Though affordability is still a challenge, these trends are early signs things might be starting to improve.

Visit my website at www.FindMauiProperty.com to search the Maui MLS and Find Helpful Resources.

It’s been a bad year for Hawai‘i Condominium Associations, with many seeing the price of their master insurance policies increasing 300% or more in one year. A few buildings saw those premiums increase by an extraordinary 900% to 1,300%.

It’s unlikely to get better any time soon.

And a growing number of condos are now carrying master insurance policies that provide less than 100% replacement coverage, which means if there’s a hurricane or other disaster, there may not be enough funds to rebuild. It’s driving some buildings to seek coverage on the pricey secondary market.

It’s creating a domino effect for everyone in “Condoland,” says Sue Savio, president of Insurance Associates in Honolulu, with condo owners, buyers, sellers and lenders all feeling the impact.

“It’s financially a serious concern,” says Savio, who estimates about 400 buildings are carrying less than 100% coverage. “I think it’s probably worse than ever.”

Rates for hurricane insurance and regular homeowner policies in Hawai‘i were already being driven up by disasters around the U.S. and the world when the deadly Maui wildfires happened last summer, putting Hawai‘i on the insurers’ radar as a wildfire state. Property and casualty insurance companies that operate in Hawai‘i pay to share their risk with the global reinsurance market, a system stressed by hurricanes and other catastrophes worldwide.

State Legislature Didn’t Intervene

The insurance woes are not limited to Hawai‘i. In California, travelers insurance recently said it would raise rates an average of 15.3% for more than 300,000 homeowners while dropping coverage for others deemed wildfire risks. State Farm had already announced it won’t renew 30,000 policyholders in California this summer. In Florida, high insurance rates and rising homeowner association fees are impacting condo sales and prices.

Hawai‘i’s Legislature tried to address the condo insurance problem during this year’s session with a bill that would have revived the Hawai‘i Hurricane Relief Fund and expanded it to allow condos to get coverage, but House Bill 2686 failed to make it out of conference committee in the last days of the session.

A condo building or complex carries a master hurricane policy to cover the cost to replace the property, which can total tens of millions of dollars in many cases, with annual premiums in the tens of thousands or even hundreds of thousands of dollars.

Over the past year, Hawai‘i condo associations have seen one-year premium increases of 300% to 600%, which is four to seven times the previous cost, says Elaine Panlilio, AOAO Group Unit manager at Atlas Insurance Agency. A few buildings are looking at increases of 10 to 14 times the amount of the previous year’s bill.

Few Standard Insurance Options

There are four standard insurance companies that write property and hurricane policies for condos according to Hawai‘i’s rules. One of those four, State Farm, will only do renewals; it hasn’t issued a new policy in Hawai‘i since Hurricane Iniki in 1992.

First Insurance Co. of Hawaii and Dongbu Insurance continue to write policies, but earlier this year, the fourth, Allianz, cut the limit on its hurricane coverage to $10 million per customer, Panlilio says.

“If you’re looking at one of the newer Kaka‘ako condos here, the replacement cost for these buildings is $300 million,” Panlilio says. “If they’re not purchasing additional hurricane layers, they only have that $10 million layer of hurricane coverage.”

Failing to maintain 100% coverage can put a building on a blacklist with lenders, which makes it difficult if not impossible for a buyer to get a mortgage on a unit. Mortgage giants Fannie Mae and Freddie Mac, both of which purchase mortgages from banks and other lenders, require coverage of 100% of a building’s insurable value, which is why many banks won’t lend on units with less than 100% coverage.

Condos can add layers of other policies to close that gap, but it’s very expensive.

For example, Panlilio says that a $300 million building with only $10 million in coverage would have to buy an additional $290 million of hurricane coverage. Those additional policy layers would cost that building anywhere from $800,000 to $1 million a year, she says.

Deferred Maintenance Is a Problem

While the overall issue with the skyrocketing rates has more to do with global disasters, the condition of individual buildings also plays a factor. If a building has had many claims, or hasn’t updated its plumbing or other aging infrastructure, the association can expect a steep hike in premiums.

Alex McLaury, an agent with ACW Group in Honolulu, points to one 10-story condo that was “riddled with water claims.” Because of that, its carrier declined to renew its insurance policy.

The condo’s premiums went from $30,000 or $35,000 under the original insurer to $200,000 on the secondary market, then about $250,000, he says. This year, the premium was $375,000. Because insurers on the secondary market are not bound by state rules or rates, they can charge more than standard carriers.

“Any building that’s currently underinsured can get insurance,” McLaury recently told a gathering of the Hawai‘i Mortgage Bankers Association. “There is still insurance available. Those (policies) especially are going to be vastly more expensive. But for the excess hurricane insurance, that is available.”

To pay those higher insurance bills, associations might raise maintenance fees, assess owners a special payment or borrow money.

“They don’t have that extra $200,000, $300,000 for insurance premiums. They didn’t budget for it,” Savio says. “Some people are assessing, others are trying to finance it, like eight, nine, 10 months of the year, but then next year’s as bad. They’re still going to be short.”

Savio says some associations say they’ll take the money from their reserve funds to pay for insurance, but she reminds them that they will have to put that money back. Others say they just won’t take the full coverage because they can’t afford it, especially those in concrete condo buildings that are more likely to withstand hurricane winds.

“I mean, I understand their thinking. And I understand everybody’s thinking on this,” she says. “And they’re hoping the Legislature will do something.”

But House Bill 2686 failed to clear a conference committee a week before the session ended on May 3. It would have revived the Hawai‘i Hurricane Relief Fund, which currently has a balance of $160 million, and opened it up to condos, and also would have added to the Hawai‘i Property Insurance Association funds.

McLaury says part of the sticker shock is a result of Hawai‘i’s property insurance rates being “artificially low for a long time.” Unlike Florida with its near-annual hurricanes and California with its frequent wildfires, Hawai‘i had been mostly free of major disasters until catastrophic wildfires swept through Lahaina and Kula on Aug. 8.

Hawai‘i tends to run one or two years behind mainland trends, says McLaury. He says he recently heard a property insurance broker from the mainland say that last year was the worst she had seen in 45 years in the insurance industry.

“I think we’re now getting into probably our worst year,” he says. Rates on the mainland have started to stabilize this year, so maybe Hawai‘i can expect to see stabilization in about two years.

However, reinsurance companies have deductibles for insurance carriers that are two or three times higher than before, he says.

Because the insurance carriers have higher deductibles of their own, “they have a greater exposure, so that greater exposure is going to mean that they’re going to have to charge more to offset that exposure,” McLaury says. “That’s one reason I don’t think we’re going to see a rate reduction for the next couple of years. I don’t think we’ll ever get back to where we were … like in 2018.

Reduces the Pool of Potential Buyers

Home sales are being affected at those 400 or so buildings that no longer carry 100% replacement coverage because most banks won’t write mortgages for units in those buildings.

“Sellers may have a di¡ cult time,” says Victor Brock, a legislative chair at the Hawai‘i Mortgage Bankers Association. “They get the pool of potential buyers diminished because it’s cash buyers, or people that can come in with bigger down payments, not the whole big pool of potential buyers. And then if someone wants to refinance, they might have very little luck.”

Meanwhile, House Speaker Scott Saiki says that while there are no plans to call a special session to deal with the insurance issue, he doesn’t rule it out. He told Gov. Josh Green that he and Insurance Commissioner Gordon Ito would monitor the situation over the summer.

“If we begin to see major impact with transactions, with the ability for people to borrow funds to purchase units, then we may have to consider it,” Saiki says. “This issue is not just about the availability and cost of property insurance but all of the ramifications which impact buyers, sellers and existing homeowners who need to insure their properties.”

Visit my website www.FindMauiProperty.com to search the Maui MLS and Find Useful Resources.

In recent years, there’s been a significant shift in how wealth is distributed among generations. It’s called the Great Wealth Transfer.

Historically, the transfer of wealth from one generation to the next was a more gradual process, often limited to smaller amounts of inheritance or family savings. But today, the scale has increased in a big way. As a recent article from Bankrate says:

“The biggest wave of wealth in history is about to pass from Baby Boomers over the next 20 years, and it’s going to have major impacts on many facets of life. Called The Great Wealth Transfer, $84 trillion is poised to move from older Americans to Gen X and millennials. If it’s managed smartly, Americans will be able to grow their wealth and ensure their financial security.”

Basically, as more Baby Boomers retire, sell businesses, or downsize their homes, more substantial assets are being passed down to younger generations. And this creates a powerful ripple effect that’ll continue over the next few decades. The graph below uses data from Merrill and Cerulli Associates to give you an idea of how much inherited money is set to change hands through 2045:

Impact on the Housing Market

One of the most immediate effects of this wealth transfer is on the housing market. Home affordability has been a concern for many aspiring buyers, especially in high-demand areas. The increase in generational wealth is expected to ease some of these challenges by providing future homeowners with greater financial resources. As assets are passed down through generations, buyers may find themselves in a better position to afford homes. Merrill talks about that benefit in a recent article:

“While millennials face steep barriers . . . to buying a first home in many markets, ‘that’s a for-now story, not a forever story’ . . . The Great Wealth Transfer should enable more of them to become homeowners — or trade up or add a second home — either through inherited property or the funds for a down payment.”

Impact on the Economy

But the Great Wealth Transfer doesn’t just impact housing. It’s also going to provide a new avenue for entrepreneurial spirits to fuel economic growth. If someone is looking to start a business and they’re receiving funds like this, that money can used as the necessary capital to start a new company. This helps the next generation of innovators and business owners bring their ideas to life.

Bottom Line

While affordability remains a challenge in today’s housing market, the ongoing Great Wealth Transfer is poised to unlock new opportunities. As wealth is passed down and put to use, it’s expected to ease some of the barriers to homeownership and fuel other entrepreneurial endeavors.

Search the Maui MLS and find Helpful Resources at www.FindMauiProperty.com

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to

Homes Are Sitting on the Market Longer: Since more homes are on the market, they’re not selling quite as fast. For buyers, this means you may have more time to find the right home. For sellers, it’s important to

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary.

Some consumers will simply wait it out before they make their purchase decision. However, it’s important to know this slowdown is small and temporary. Home Prices

Home Prices